CEL-SCI ($CVM ) - Bought Deal, Successful Liquidity Risk Mitigation Measure

My opinion, no investment advice

A. Summary

CEL-SCI announced a bought deal of 1,000,000 shares, then up-sized to 1,400,000 shares, raising $29.5m before green-shoe and up to $34.0m after green-shoe exercise.

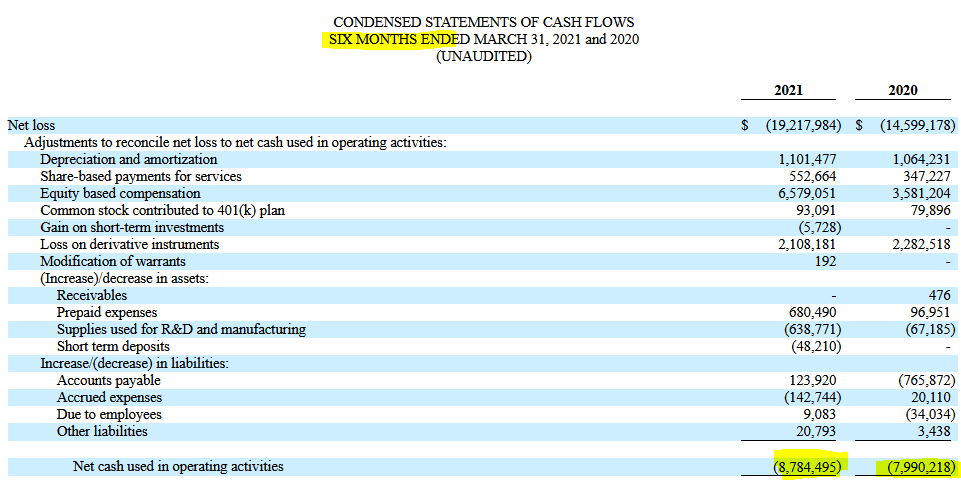

CEL-SCI’s cash burn is $4m per quarter. CEL-SCI had $17m cash and liquid asset at end of Q1 2021 or enough cash until Q1 2022. The cash raise secures liquidity until end of 2023 at current burn rate. This does not look like a data release timeline, but more like an FDA approval timeline.

For a price of 3% dilution, the cash raise is an insurance, a risk management measure in the unlikely scenario that Phase 3 trials fail to show strong statistical significance on survival benefit; or any unforeseen risks that require cash.

The cash raise does not mean data release is far away.

B. The Bought Deal

This bought deal is a typical underwritten offering. Kingswood was the sole underwriter who bought shares from CEL-SCI at $21.04/share and sold them to investors at $22.62/share. Let’s take a closer look at the process.

At 4:57pm, June 8, CEL-SCI announced the signing of an underwriting agreement to sell to Kingswood a minimum of 1,000,000 shares at public price of $22.62 per share, or 5% discount to CEL-SCI’s closing share price of the day. Kingswood has 30-day option to buy up to 150,000 additional shares (green-shoe option)

Note that $22.62 is the price Kingswood would sell to investors, not the price it bought shares from CEL-SCI which was $21.04/share.

In order to obtain this public price, Kingswood would likely have tested the water before. That means between market close at 4:00pm and 4:45pm, Kingswood and CEL-SCI would likely have wall-crossed several core and close-relationship investors. Those investors would sign a Non-Diclosure Agreement and would be offered 1-1 call with Geert in which Geert would explain the rationale of the raise.

After the wall-cross, some investors would put some orders, making Kingswood and CEL-SCI confident to announce a public price of $22.62.

CEL-SCI and Kingswood signed the underwriting agreement and announced it publicly.

After 4:57pm, the bought deal was public, Kingswood would call more investors to market the deal more broadly.

The marketing effort brought some fruits. Kingswood filled the order book. At 9:26pm, CEL-SCI announced an 40% up-sizing of the deal to 1,400,000 shares with a green-shoe option of 210,000 shares.

In the morning of June 9, Kingswood sold 1,610,000 shares at $22.62/share to investors who put in total $36.4m into this deal.

Note that Kingswood would short sell 210,000 shares they had not owned yet.

During 30 days following the offering, if the CEL-SCI share price increase to above $21.04, Kingswood will exercise its option to buy 210,000 shares from CEL-SCI at $21.04 to cover its short position.

On the contrary, if the CEL-SCI price decreases to below $21.04, Kingswood will buy share from the open market to cover its short position.

In either case, they are making money on the green-shoe.

Overall, a tight discount of 5% of public price vs. daily closing price and the 40% up-sizing suggests the marketing of the deal went well and investors putting 36.4m to buy had received some reassuring insights from Geert.

C. Clarifying Longs’ Doubts

The cash raise was a big surprise for many longs, and cause understandable confusion. Here are the common questions.

1. Does CEL-SCI raise cash to survive until data release?

Short answer, no. Let’s take a look at the Q1 2021 10-Q which says:

Total cash and U.S. treasury bills of $17.5m

Cost of the facility upgrades is $10.6m of which $9.5m already incurred end of Q1

Cash burn of $8m for 6 months period, or $4m per quarter

This means CEL-SCI does not expect material investment in fixed-asset after Q1, have enough cash for 4 quarters starting from end of Q1 or until Q1 2022. So CEL-SCI did not raise cash to survive until data release, or at least did not need to raise cash now to survive until data release.

The amount of cash raised is between $29m to $34m (including green-shoe) or 7 to 8 quarters of cash burn. Combining with existing cash, CEL-SCI has enough cash until end of 2023. No way this corresponds to the timing of data release.

2. Why raising cash now and not waiting until after data release if it’s very close and Geert is very confident?

Several points here.

3% dilution does not matter for Geert. What matters for him is the success of Multikine and his net-worth will go from what he has now to $1bn, and not whether it will be $1bn or 1.03bn. As for all longs, do we really care if the ultimate price of CEL-SCI is $200 or $206; $400 or $412? 3% is plain noise.

There are 2 scenarios where this cash raise is useless:

Multikine is an undiscussable success meeting all primary and secondary endpoints. Then the market cap of CEL-SCI would be multiple of where it is now. Raising cash would be the least issue it will have.

Multikine is an undiscussable failure, failing to meet primary and secondary endpoints. Then CEL-SCI will join the graveyard of failed biotechs. $40m cash at hand and LEAPS will not help them survive. Geert would lose 100% credibility, Adam will become a hero, and there is no way for Geert to raise capital to develop LEAPS.

But there are 1 scenario, neither black nor white, a gray one, in which the cash could be useful which is: Multikine shows a borderline statistical significance (e.g. p-value between 0.05 and 0.2) but meets some of secondary endpoints (e.g. tumor reduction). Imagine what would happen after such a scenario:

CEL-SCI might need to perform additional work to provide more evidences of survival benefits and need money for that.

The shorts will attack, telling that Multikine is a failure and Geert is trying to data mine to show some benefits with hope of FDA approval.

The share price would not go to $0 but single digit $, and make it difficult to raise cash without material dilution.

Buy-out candidate could find some interests, but can leverage CEL-SCI’s weak financial position to negotiate a good price, saying that FDA approval is not a sure thing, etc.

Hence, by having $40m cash on its bank account, CEL-SCI could still go until FDA approval, avoid the consequence of short attack, and strengthen bargaining power vs. big pharma. So why not raise cash now? It does not cost anything to Geert, and remove a risk for him.

Now the key question is whether it is only a risk management measure, or whether Geert has learnt something about the primary end point results? Only g*d knows. I personally think it is the former: Geert is a lawyer and he knows the limit. If he learnt some not so great news about the primary end points and still decided to do an offering without disclosing the news, he will take a serious risks in case of litigation.

In addition to this gray scenario, having cash also helps CEL-SCI cope with any risk that requires cash. The liquidity risk is now gone. Data is the only thing that matters now.

3. Why’s the Cash Raise Does Not Mean Data Is Far Away?

Many longs think the cash raise means data is still very far away. Not necessarily.

Remembers the investors / funds putting $36.4m in the bought deal? Remember the up-sizing of the deal? Let’s not assume those investors are random, stupid guys. They actually have more information than most of us. Yet they put a lot of money in the deal. Do you think it would be rationale for them to do that if data is still very far away? They would ask the same usual questions to Geert. When will be the data lease? What’s your view about the results? Why are you raising cash now? The success of the deal makes me think Geert’s speech was the one he has been giving so far: “Data soon, likely good results, raise cash eliminate liquidity risk and show strong positions to big pharma .”

Another point, take a look at the 8-K filed on June 9 which described the bought deal. There is a key lock-up clause:

The agreement of the Company not to sell any of its securities and the agreements of the Company's officers and directors not to sell or transfer any of the Company's securities for this 30 day period will not apply after the Company publicly discloses the results of its Phase III clinical trial.

That means, during 30 days following the bought deal, CEL-SCI’s officers and directors cannot transact on shares / securities of CEL-SCI unless the Phase III results are announced. If data were months away, they probably would not need this clause.

D. Conclusion

The bought deal has raised some doubts and noises among longs but could be well a simple risk management measure of Geert against mid-term liquidity risk. It does not mean data is very far away. There is no real reason for longs to be over-worried by this bought deal. On the contrary, CEL-SCI has more than 2 years of cash now. The liquidity risk has been eliminated.

I’m long CEL-SCI. Investing in biotech is complex and risky. Do your work before making investing decision and do not take my analysis as advice.

Great Article to read and touched both short and long side. Great work Andy.

Well done, Andy. Very well done.